Health insurance in the United States is changing, and the change is coming to the State of California sooner than anywhere else. In coming months, the issues are going to move beyond politics and talk radio, and become a real part of your real life.

It may seem like a daunting topic to dive into, especially if you have not been following it closely for the past two-and-a-half years. Many politicians are so divided over the legislation that it is hard to know whom to believe, and much of the industry information is saturated in complicated language.

With just over a month before open enrollment begins in California, however, it is time to figure out what changes are really happening, and how it affects you and your family.

Table of Contents

- History of the Affordable Care Act and Covered California

- The Ongoing Healthcare Debate

- From Talking Points to Real Life

- Specialized Applications

- Your Next Steps

History of the Affordable Care Act and Covered California

The Patient Protection and Affordable Care Act is the official title of the new laws that are about to change health care in the United States. You may have also heard it referred to as:

- The Affordable Care Act (or ACA)

- Health Insurance Reform

- Health Care Reform

- Obamacare

This reform has been in the works for about four years, since it was introduced in the House of Representatives on September 17, 2009. Here is a brief history of the national law, and how it came to California:

-

September 17, 2009 – Introduced in the House as “Service members Home Ownership Tax Act of 2009,” (H.R. 3590) by Charles Rangel (D-NY)

-

October 8, 2009 – Passed the House, 416-0

-

December 24, 2009 – Passed the Senate, 60-39, as “Patient Protection and Affordable Care Act,” with amendment

-

March 21, 2010 – House agreed to Senate amendment, 219-212

-

March 23, 2010 – President Barack Obama signed into law

-

June 28, 2012 – Supreme Court upheld most of the law in National Federation of Independent Businesses v. Sebelius, 5-4

-

September 30, 2012 – Governor Schwarzenegger signed two bills – AB 1602 and SB 900 to create the California Health Benefit Exchange

This past October, the board of the California Health Benefit Exchange established the more consumer-friendly moniker Covered California.

In short, Covered California is how the Affordable Care Act – a.k.a. Obamacare – is coming to California.

The Ongoing Healthcare Debate

Even though the reform is moving forward, there is still a lot of debate and disagreement surrounding it. The two main focuses of this debate are:

-

The legality of the ACA

-

The financial impact of the reform

Legality of the Affordable Care Act

Those opposed to Obamacare have argued that law is unconstitutional because of what became known as the “individual mandate.” The individual mandate is the part of the bill that requires everyone to have some sort of health insurance coverage, or pay a penalty. Opponents questioned the legality of the federal government requiring private citizens to purchase health insurance.

These arguments were largely put to rest in June of 2012, when the Supreme Court of the United States (SCOTUS) upheld most of the law. SCOTUS decided that the individual clause is a tax, not a mandate, and that individual states cannot be required to participate in the ACA.

Since June 2012, two new contentions have surfaced based on the legality of the law:

-

All taxes must originate in the House of Representatives

-

A new IRS rule on federal subsidies

Taxes Originate in the House

In September 2009, the House of Representatives passed the Home Ownership Tax Act. When the bill went to the Senate, it was amended and renamed the Patient Protection and Affordable Care Act. In March 2010, the House agreed to the Senate’s changes. The bill as the ACA, then, originated in the Senate.

None of that would have mattered until the Supreme Court, in their June 2012 ruling, declared that the “individual clause” is a tax. The U.S. Constitution requires that, “all bills for raising revenue shall originate in the House of Representatives.”

IRS Rule: The ACA’s Impact on the National Deficit

No one wants the ACA to add to the national deficit. To avoid this, the law would be implemented by state governments, in state-run exchanges, shifting the cost of the program to the state governments. If a state declined participation in the ACA, the federal government would then be forced to set up a federal exchange to offer consumers in that state.

Since the Supreme Court ruled that states cannot be required to participate, federal subsidies were offered as incentive. Low-income consumers, who purchase their health insurance through a state-run exchange would be eligible for federal subsidies. Section 1321 of the law deals with the federal exchanges, and does not allow these subsidies to consumers in a federal exchange.

However, 34 states have decided not to set up state exchanges, which leaves a lot of health insurance reform up to the federal government to fund. The IRS – on May 23, 2013 – established a rule allowing subsidies for consumers in federal exchanges anyway. Opponents argue that the IRS does not have statutory authority to change laws.

The state of Oklahoma has filed suit against the federal government to establish that point.

The ACA’s Financial Impact

The financial impact of the ACA is still being discussed on an individual and a national level. Rates are being released in a few states, including California, who have already set up state exchanges, but it may be hard to assess the change until enrollment actually begins.

Affordable Care Act’s Impact on Individual and Family Finances

Economists and politicians have been arguing for years whether the ACA will make healthcare more or less affordable for the average consumer.

Supporters argue that healthcare will become more affordable for the average individual and/or family for several reasons:

-

50+ million new customers buying new health insurance policies will drive prices down as insurers compete for new business.

-

Tax credits and federal subsidies will reduce the actual out-of-pocket expenses for many.

-

The program pays for itself by turning the penalties collected back into financial support.

Opponents maintain that insurance rates will increase for the average consumer for two reasons:

-

Insurers are now required to accept everyone, and more people who require expensive medical treatments will drive the cost of medical care higher.

-

Insurers are now required to provide “essential health benefits,” including things like prenatal and maternity care, from which consumers could previous opt out.

National Financial Impact of the ACA

In September of 2009, President Obama told a joint session of Congress:

“First, I will not sign a plan that adds one dime to our deficits – either now or in the future.”

However, opponents are now saying that because over half of the states have refused to set up state exchanges, the federal government will be forced to bear the majority of the expense to set up federal exchanges for consumers in those 34 states.

From Talking Points to Real Life

While debate rages and lawsuits are filed, however, health care reform marches on, especially in the state of California, where open enrollment is slated to begin in October, 2013. So what is actually happening?

Here are the three big things you need to know:

-

What is changing? – There are new requirements of, and restrictions on, insurers.

-

How is it going to work? – Coverage will be offered in four tiers.

-

How does it apply to you? – As an individual, a family, a small business, and as a senior citizen.

The Affordable Care Act’s New Requirements

The ACA makes some new requirements of health insurance providers, effective immediately, including:

-

Essential Health Benefits

-

Protection of physician-choice

-

Dependents can stay on their parents’ plan until they are 26 years old.

Essential Health Benefits

Obamacare requires every plan offered by every insurer to include “essential health benefits.” These are items and services within at least 10 categories:

-

Ambulatory patient services

-

Emergency services

-

Hospitalization

-

Maternity and newborn care

-

Mental health and substance use disorder services, incl behavioral health treatment

-

Prescription drugs

-

Rehabilitative and habilitative services and devices

-

Laboratory services

-

Preventative and wellness services and chronic disease management

-

Pediatric services, incl oral and vision care

“Preventative services” includes contraception, unless the employer is a church or house of worship. Other details about each category will vary by state.

Protection of Physician-Choice

Your right to choose your own medical providers is protected (for policies written after March 23, 2010) by the ACA in three ways:

-

You can choose any doctor and/or pediatrician in your plan’s network.

-

Women do not need a referral before visiting an OB-GYN.

- You can get emergency medical services outside of your network without higher co-payments or coinsurance, and without being required to obtain prior approval from your insurer.

New Restrictions

In addition to new requirements, the law also now prohibits the following:

-

Price discrimination based on pre-existing conditions

-

Price discrimination based on gender

-

Annual or lifetime limits on health care

-

Dropping policy-holders when they become sick

Further, Obamacare prohibits insurance companies from unnecessary price increases:

“Insurers must justify premium increases. Insurance companies are required to spend 80 percent of premium dollars on quality health care, not administrative costs like salaries and marketing.”

Coverage Level Tiers

Starting in 2014, insurance providers will have to provide policies that conform to four tiers of coverage, with a choice of plans in each tier:

-

Platinum – Covers 90% of medical expenses, for the highest premium rate

-

Gold – Covers 80% of medical expenses, for a moderately-high premium rate

-

Silver – Covers 70% of medical expenses, for a moderate premium rate

-

Bronze – Covers 60% of medical expenses, for a moderately low premium rate

In California, multiple companies have been chosen to work with the Covered California exchange:

-

Anthem Blue Cross of California

-

Blue Shield of California

-

Chinese Community Health Plan

-

Health Net

-

Kaiser Permanente

-

L.A. Care Health Plan

-

Molina Healthcare

- OSCAR Health Plan of California

-

Sharp Health Plan

-

Valley Health Plan

-

Western Health Advantage

These 11 companies will all offer a variety of plans in each of the four tiers. Premiums will vary within the tiers, but coverage will not. This will allow consumers to easily shop for the best health insurance policy in their budgets, by creating a simple way to compare apples to apples. It will be like shopping for the same car at 11 different dealerships.

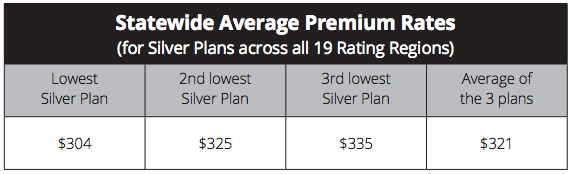

The following table from Covered California shows an overview of average premium rates for Silver plans across the state:

In addition to these four metal tiers, some consumers may be eligible for a Catastrophic plan. These plans:

-

Cover Essential Health Benefits

-

Have a high deductible, but a lower premium than the Bronze plans

-

Are only available to individuals under 30, or those who have been exempted from the individual mandate because there’s no affordable coverage

How Does Covered California Apply To You?

Now it’s time to get specific. What is Covered California going to mean to your life as:

-

An individual or family?

-

A senior citizen?

-

A small business?

Covered California for Individuals and Families

First of all, if you already have insurance, you don’t really have to do anything. Covered California may be a benefit to you, though. Here are some things to consider.

If you get insurance coverage through your job, and you pay more than 9.5% of your household income toward premiums, you may be eligible for financial assistance through Covered California. Covered California will look at your existing coverage if you apply, and determine if your current coverage is adequate and affordable.

If you currently pay for your own health insurance, you may be eligible for financial assistance. You must purchase a new plan through Covered California to qualify for that assistance.

If you do not have health insurance, you may either purchase a health insurance plan through Covered California during open enrollment, or pay a penalty at tax-time. The amount of the penalty will increase every year, but will never exceed the national average of a Bronze-tier premium.

For the next three years, the uninsured will pay a percentage of their income, or a flat fee, whichever is greater:

-

2014 – 1% or $95

-

2015 – 2% or $325

-

2016 – 2.5% or $695

There are exemptions. People who qualify for the following exemptions would not be required to purchase health insurance or pay a penalty:

-

Those who would pay more than 8% of your income for the lowest premium rate

-

Those whose income is below the requirement for filing taxes ($9750 single, $27,100 married with two kids – 2012)

-

Those qualifying for religious exemptions

-

Undocumented immigrants

-

The Incarcerated

-

Native American tribal members eligible for care through a Native American health care provider

Religious exemptions include:

-

Members of religious sects already exempt from Social Security requirements, such as the Amish or Mennonites

-

Members of health care sharing ministries

Covered California for Senior Citizens

The ACA improves health care for senior citizens in many ways, including:

-

Closing the “donut hole” – the gap in prescription drug coverage in Medicare Part D – by 2020

-

Free annual check-ups

-

Eliminating deductibles and co-payments for preventive care in Medicare

The reform also adds safeguards and protections for seniors in nursing homes and assisted living facilities:

-

Establishes Elder Justice Act to prevent and eliminate abuse, neglect, exploitation

-

Creates standardized complaint form for nursing homes

- Establishes nationwide program for national and state background checks for employees

Covered California for Small Businesses

Covered California divides small business into two categories, based on their sizes: those with one to 49 employees, and those with 50 to 100 employees.

Small businesses with fewer than 50 “full-time equivalent” employees do not need to provide health insurance. Any of these businesses that choose to provide health insurance anyway may qualify for tax credits if they meet the following criteria:

-

Fewer than 25 full-time equivalent employees, paid less than $50,000/year average

-

AND employer pays 50+ percent toward employee’s premium

Businesses with 10 or fewer full-time equivalent employees, who are paid $25,000/year or less, are eligible for the maximum tax credit.

Non-profits and tax-exempt employers have to meet the same requirements to be eligible for tax credits, but their credits will be lower.

Small businesses with 50 or more full-time equivalent employees will be required to provide health insurance, or may face penalties starting in 2015.

Employers that do provide insurance will still maintain control over what level of insurance is offered. The employer will select the metal tier they are willing to offer, and employees will be able to select from available plans within that tier.

-

Businesses with less than 50 employees can buy insurance this fall that will start in January 2014. Businesses with 50 to 100 employees can buy insurance in October of 2015, that will start January 2016.

Specialized Applications

No two people – and no two families – have the same health care needs. Health insurance can be a particularly difficult subject to navigate for people with pre-existing medical conditions, and for low-income individuals and families.

Pre-Existing Conditions

Starting in 2014, no one can be refused health insurance coverage. For people with pre-existing conditions, this means:

-

Insurers cannot charge different rates based on health status.

-

There will be no lifetime limits.

There has, traditionally, been some wrangling over the definition of the term “pre-existing condition” for insurance purposes.

However, once the law takes full effect in 2014, that definition will lose its importance. Under the law, no one can be denied health care insurance for any reason, including an existing medical condition. – WebMD

Low-Income Individuals and Families

The ACA makes two provisions for financial assistance:

-

Tax credits

-

Federal subsidies

Tax Credits Available Within Covered California

Tax credits are available to low- and middle-income individuals and families, based on a sliding scale. Tax credits are applied at the time of enrollment, to reduce premium cost. Consumers will not need to wait until filing a tax return at the end of the year to see these savings.

If you currently have health insurance, you can still apply for the tax credit. If you pay for your health insurance yourself, and your family qualifies, you will be able to purchase a new insurance plan through Covered California to claim the tax credit. If you currently receive health insurance benefits through your employer, Covered California will analyze your coverage. If the coverage you receive through your employer is deemed adequate and affordable, you will not be able to claim the tax credit through a new plan with Covered California.

Federal Subsidies Available Within Covered California

Cost-sharing subsidies are an additional benefit to qualifying families. Also calculated on a sliding scale, cost-sharing subsidies are applied to lower your cost at the time you or a family member receives care.

Your Next Steps

Now that you know where Health Care Reform has come from, and where it is going, you are in a great place to make the best decisions for your and your family.

Covered California will open enrollment from October 1, 2013, through March 31, 2014. Coverage will begin January 1, 2014, or when you start a new policy.

Here are a few tips and steps to help you get ready for open enrollment:

-

Set your budget – You will need to know how much you want to spend each month on premiums.

-

Ask your employer if he/she plans to offer insurance in 2014.

-

Make sure you understand how coverage works, including premiums, deductibles, out-of-pocket maximums, co-payments and coinsurance.

If you have any questions, or you are still unclear on how coverage works, we would love to help. Call 800-585-1776 or send an email to [email protected].